Bharat Coking Coal IPO Lists at 96% Premium: Market Verdict Defies GMP Cool-Off

Author

Bharat Coking Coal Limited listed today, January 19, 2026, at a bumper 96% premium over the IPO price of ₹23 on both NSE and BSE. The sharp debut significantly outperformed grey market expectations, reinforcing strong institutional and retail confidence in BCCL’s strategic importance, dominant coking coal position, and long-term relevance to India’s steel and infrastructure ecosystem.

Bharat Coking Coal IPO Overview

The BCCL IPO opened on January 9, 2026, and closed on January 13, 2026. It was a ₹1,071 crore issue, structured entirely as an Offer for Sale by Coal India. The price band was fixed at ₹21–₹23 per share, with a lot size of 600 shares, translating to a minimum investment of ₹13,800 at the upper band.

As a pure OFS, the IPO did not raise fresh capital for the company. Instead, it enabled partial monetisation of a strategic PSU asset while bringing BCCL to the public markets.

Why BCCL Matters

BCCL occupies a uniquely critical position in India’s industrial ecosystem. It accounts for nearly 58.5% of India’s domestic coking coal production, making it the backbone supplier to the country’s steel industry. Coking coal is an essential input for steelmaking and has limited substitutes, giving BCCL structural relevance as India continues to expand infrastructure and manufacturing capacity.

The company operates 34 mines across the Jharia and Raniganj coalfields, with coal reserves estimated at close to 7,900 million tonnes. Its key customers include SAIL, Tata Steel, and JSW Steel, anchoring its revenues to long-term steel demand.

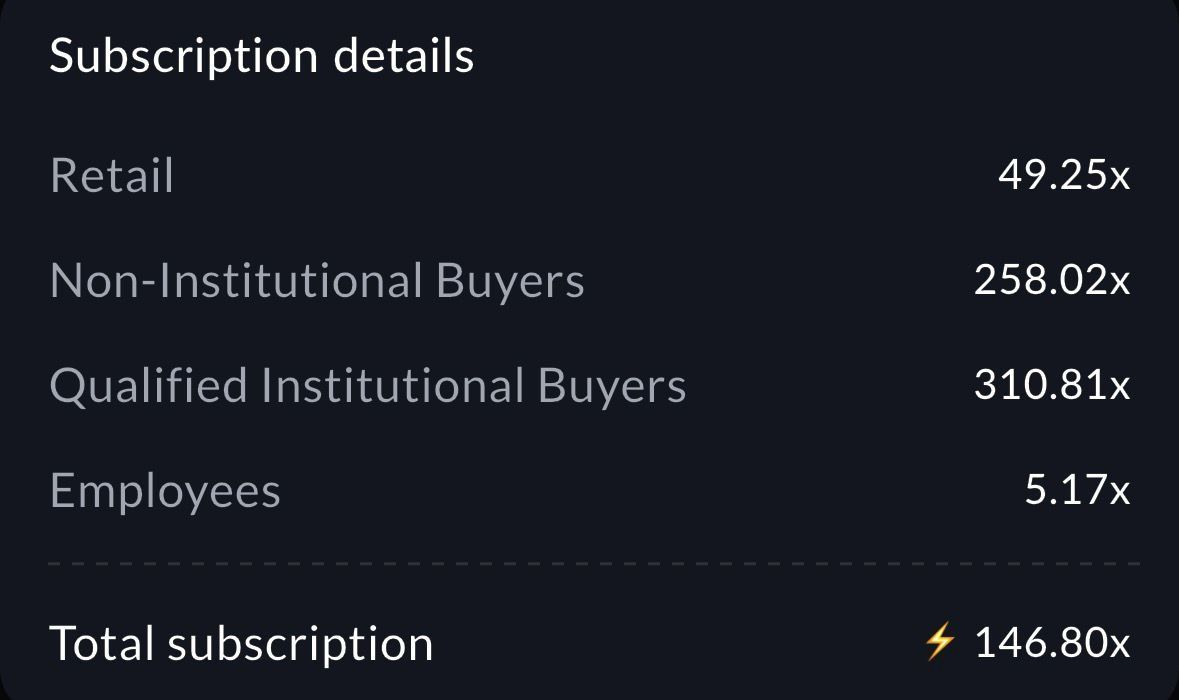

Subscription and Institutional Interest

Investor appetite for the IPO was extraordinary. Overall subscription crossed 146×, with institutional demand exceeding 300×, supported by strong participation from non-institutional and retail investors as well. The book built steadily over the issue period, indicating conviction rather than last-minute frenzy.

Anchor investors reinforced this confidence. BCCL raised ₹273 crore from anchor investors at the upper band, with participation from LIC and multiple domestic mutual fund houses. This institutional backing played a key role in sustaining the IPO premium even as grey market sentiment cooled.

Financial Snapshot

Bharat Coking Coal Limited (₹ crore)

| Particulars | FY23 | FY24 | FY25 |

|---|---|---|---|

| Revenue | 13,019 | 14,653 | 14,402 |

| EBITDA | 891 | 2,494 | 2,356 |

| Profit After Tax | 665 | 1,564 | 1,240 |

| Total Assets | 13,313 | 14,728 | 17,283 |

What this tells us:

FY24 captures peak-cycle profitability driven by elevated coal prices, while FY25 reflects normalisation rather than deterioration. Despite softer realisations, BCCL remains cash-generative and maintains a conservative balance sheet characteristic of a mature PSU miner.

Valuation Snapshot

Bharat Coking Coal Limited (at upper band ₹23)

| Metric | Value |

|---|---|

| Issue Price | ₹23 per share |

| Implied Market Capitalisation | ~₹10,711 crore |

| FY25 Earnings (PAT) | ~₹1,240 crore |

| EV / EBITDA (annualised) | ~16× |

| Coal India P/E (approx.) | ~8–10× |

What this tells us:

BCCL is listing at a clear premium to Coal India, reflecting its focused exposure to coking coal and strategic importance in the steel value chain. However, the valuation already prices in strong profitability, leaving limited margin for error if coal prices weaken or steel demand slows, a key reason behind the cooling GMP.

BCCL IPO Listing Expectations

With grey market premiums moderating but demand remaining strong, expectations have reset. A weak listing appears unlikely, but so does an explosive debut. A steady listing in the ₹30–₹35 range appears reasonable, balancing institutional support with valuation sensitivity.

Post-listing performance will be driven less by IPO sentiment and more by coal pricing trends, steel demand momentum, and broader PSU market sentiment.

Key Risks to Watch

BCCL’s earnings are inherently cyclical and sensitive to coal price movements. Any slowdown in steel demand can directly impact volumes and margins. Environmental and regulatory pressures around mining remain a structural risk, while PSU ownership adds stability at the cost of operational agility.

Sahi’s Verdict

Subscribe for Long Term | Avoid Pure Listing Flips

BCCL is not a momentum IPO. It is a strategic, cycle-linked PSU play tied closely to India’s steel growth story. Long-term investors who understand commodity cycles may find value in holding through volatility. Short-term traders should track listing-day price behaviour closely and avoid chasing strength driven purely by IPO hype.

Related

Orkla India IPO Allotment Status, Subscription & Listing Details

Canara Robeco AMC IPO Allotment Status, Subscription & Listing Details

Aequs IPO Listing Sees 101.63× Subscription Ahead of Listing

Fujiyama Power Systems IPO Allotment Status: How to Check

Recent

What is an IPO & How to Apply for an IPO on Sahi: Step-by-Step Guide

Indicator Templates: Build Once. Trade Faster Forever.

Pledging in Trading: How Traders Use Their Portfolio as Trading Capital

How to Read the Option Chain to Predict Market Moves in Weekly Expiries?